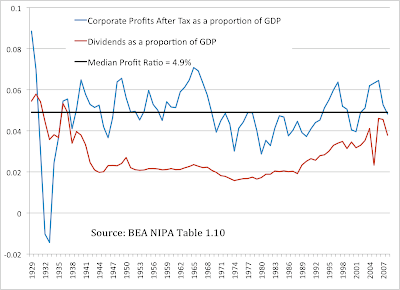

Earlier I mentioned how the market cap growth of companies cannot outpace GDP growth -- except for brief periods of multiple expansion. Here is a chart from 1929 to 2008 showing the total net operating profits after taxes together with dividend payouts of U.S. Corporations divided by Gross National Income (the data comes from the BEA):

Over this time period, the ratio of profits available to corporate business was around 5% of the economy. There is what seems to be obvious mean-reversion. More interesting is the stability of the dividend payouts except for the two credit bubble periods, one deflating since 1929, and one inflating from the 1980s until just recently. Companies are loathe to increase dividends without appropriate future coverage, and so the dividend payout/GNI contains meaningful information about the estimates of management for sustainable future returns, and is much less volatile than the equity multiple. A dividend payout of 2% of GNI was remarkably stable between the two credit bubbles.

Early data about market capitalization is hard to find, but we can look at total market capitalization in the second half of the 20th century. The following chart, from the Federal Reserve Flow of Funds, shows total market capitalization of U.S. corporations divided by the Gross National Income, reported on a quarterly basis. You can also see the total dividend payouts divided by the total market cap (i.e. the dividend yield of the entire market).

By this historical metric, the present market is not cheap. It would need to fall by 50% in order to reach the post-war lows from 1974-1984 -- and that is a decade long period! We can also see the same shape that is a common refrain in most of the graphs: the 20 year run-up culminating to the twin-peak blow off of 2000 and 2007 that at least seem to suggest the beginning of a downtrend. From this long-run perspective, the period from 2003-2007 seems like an enormous bear market rally.

Don't let anyone fool you into believing that the total equity value of U.S. corporations can consistently outpace the size of the economy. As can be seen from the historical record, periods of multiple expansion for both corporate profits/GNI as well as market-cap/GNI tend to mean-revert, even though they can last long enough to convince the public that "this time it's different". Those who cut their teeth in the period from 1980-2000 did not experience a representative time in the history of U.S. equity values.

Historically, the Market Cap of U.S. Corporations averaged approximately the size of GNI (actually 0.94xGNI), although it did swing around this value. The following chart shows the actual 10 year returns of purchasing a slice of equity, together with the predictions of 2 estimates.

The 10-year forward equity returns have been the worst on record in the postwar period.

The first estimate assumes 100% reversion in a 10 year time period, with the assumption that GDP growth will be the value of the current 10 year treasury. The second line assumes 50% reversion to the 0.94xGDP value, also assuming that 10 year forward GDP growth will be equal to the 10 year treasury rate. Of course, no one can tell when or to what extent mean-reversion will occur. This type of analysis is a crude version of

John Hussman's analysis, with the notable exception that I am using the 10 year treasury estimate of GDP as opposed to a constant 6% GDP growth trend, I'm excluding dividends in the total return calculation, and am selecting the parameters not by fixed P/E terminal multiples, but by proportion of trend reversion. The interested reader can make each of these adjustments themselves -- the purpose here is not to predict market values, as it is hard to out-guess the crowd, but to provide a sense of valuation for the market as a whole -- what does a dollar of equity buy today in comparison to what it bought yesterday? Moreover, if the present multiples were to mean-revert, then what would the market cap be? These types of considerations should inform those who don't always believe that we are in a new era.

Both estimates currently predict annualized returns of approximately 3% (excluding dividends), over a 10 year period. These are all nominal returns, but the Old Barkeep is not too worried about inflation over the next decade. I hope to return to this theme with some more sophisticated models.

No comments:

Post a Comment