Thursday, December 17, 2009

Friday, December 4, 2009

Thursday, December 3, 2009

Egads! Winterspeak is shocked

In a post entitled winterspeak.com: Banks are even more super than I thought, Winterspeak is groping towards an understanding of what it means for balance sheets to expand, and the role of money in funding investments (it doesn't).

The idea that banks fund themselves by expanding their balance sheets is not unique to banks -- that is how all investment works for both bank and non-bank entities.

The only super thing about banks is that they have below market funding costs and access to government overdraft facilities that allow them to evade market pricing of assets. Banks can jump in and out betwee mark-to-market (when it suits them) and mark-to-model (when it suits them better).

Investment is not funded by savings, but by expectations of future returns, discounted by opportunity cost (e.g. by all other return prospects). The role of savings (== profits, as flows), is to help price financial claims against each other. E.g. if one investment pays out $1/share each month and another investment pays out $2/share each month, then the share prices of both investments are adjusted so that the risk-adjusted cash-flows of both investments are equal.

For example, suppose I have a bright idea to make money in real estate, or giving massages to former Soviet Hockey players. It doesn't matter what the idea is, I want to float bonds (or equity). So I am willing to assume a financial obligation:

All I have now is a piece of paper -- a promise. I then sell my paper to the financial markets. In exchange for this promise I obtain cash to buy a new massage table or a shopping center in the desert, as the case may be.

How does my investment get funded?

An investor holds money in a money market account, that is backed by treasuries. The investor liquidates this account and buys my paper. I take the proceeds from the investor and put them into a money market account, backed by the same treasuries that the investor sold.

For every buyer there is a seller. In this case, I sold my paper and bought treasuries, and the rest of the market (by identity) had to sell me treasuries and buy my paper. We just made an exchange, in which both treasuries and paper were priced in terms of cash and then an equal amount of one was exchanged for the other.

The whole thing could be achieved if the economy contained only 1 ruble (and advanced settlement software). I could raise hundreds of billions in ruble assets even if only a single ruble exists in the whole world. Money is not used up in the buying and selling of financial claims, and money does not fund investments, rather financial claims are all priced in terms of money.

In this way, the portfolio of the investor did not increase or decrease as a result of making the investment. All that happened was they he shifted his portfolio holdings in a way to reflect his return expectations. Tomorrow, he could sell his claim on me and instead buy treasuries again. In the process of doing so, the price of my paper my rise or fall in relation to treasuries, and therefore the investor can suffer a gain or loss on the investment.

The only way that an investor can profit from financial transactions is via capital gains or losses, as the present value of dividend and interest payments (discounted by opportunity cost) are already reflected in the price of the asset. It is only misperceptions of this present value that can enrich or impoverish an investor.

Therefore investments are funded by an expectation of future profits. They are not funded by savings (=profits accumulated in the past).

The only special thing about banks is that they have government backing and government-set cost of funds, whereas private investors have to pay the market price for funds. When a private investor wants to buy an asset with leverage, he must pay the market price for funds, whereas a bank is able to pay the government-set price for funds. That, and a lot of subsidies + direct phone calls to Treasury, is the only difference between banks and non-banks :)

The idea that banks fund themselves by expanding their balance sheets is not unique to banks -- that is how all investment works for both bank and non-bank entities.

The only super thing about banks is that they have below market funding costs and access to government overdraft facilities that allow them to evade market pricing of assets. Banks can jump in and out betwee mark-to-market (when it suits them) and mark-to-model (when it suits them better).

Investment is not funded by savings, but by expectations of future returns, discounted by opportunity cost (e.g. by all other return prospects). The role of savings (== profits, as flows), is to help price financial claims against each other. E.g. if one investment pays out $1/share each month and another investment pays out $2/share each month, then the share prices of both investments are adjusted so that the risk-adjusted cash-flows of both investments are equal.

For example, suppose I have a bright idea to make money in real estate, or giving massages to former Soviet Hockey players. It doesn't matter what the idea is, I want to float bonds (or equity). So I am willing to assume a financial obligation:

To pay the bearer of this instruments 10 rubles a week.

All I have now is a piece of paper -- a promise. I then sell my paper to the financial markets. In exchange for this promise I obtain cash to buy a new massage table or a shopping center in the desert, as the case may be.

How does my investment get funded?

An investor holds money in a money market account, that is backed by treasuries. The investor liquidates this account and buys my paper. I take the proceeds from the investor and put them into a money market account, backed by the same treasuries that the investor sold.

For every buyer there is a seller. In this case, I sold my paper and bought treasuries, and the rest of the market (by identity) had to sell me treasuries and buy my paper. We just made an exchange, in which both treasuries and paper were priced in terms of cash and then an equal amount of one was exchanged for the other.

The whole thing could be achieved if the economy contained only 1 ruble (and advanced settlement software). I could raise hundreds of billions in ruble assets even if only a single ruble exists in the whole world. Money is not used up in the buying and selling of financial claims, and money does not fund investments, rather financial claims are all priced in terms of money.

In this way, the portfolio of the investor did not increase or decrease as a result of making the investment. All that happened was they he shifted his portfolio holdings in a way to reflect his return expectations. Tomorrow, he could sell his claim on me and instead buy treasuries again. In the process of doing so, the price of my paper my rise or fall in relation to treasuries, and therefore the investor can suffer a gain or loss on the investment.

The only way that an investor can profit from financial transactions is via capital gains or losses, as the present value of dividend and interest payments (discounted by opportunity cost) are already reflected in the price of the asset. It is only misperceptions of this present value that can enrich or impoverish an investor.

Therefore investments are funded by an expectation of future profits. They are not funded by savings (=profits accumulated in the past).

The only special thing about banks is that they have government backing and government-set cost of funds, whereas private investors have to pay the market price for funds. When a private investor wants to buy an asset with leverage, he must pay the market price for funds, whereas a bank is able to pay the government-set price for funds. That, and a lot of subsidies + direct phone calls to Treasury, is the only difference between banks and non-banks :)

More on wage shares in OECD

Data source for wages:

http://www.oecd.org/document/63/0,3343,en_2649_33729_38939455_1_1_1_1,00.html

GDP/capita taken in current prices from OECD country statistical profiles.

Wednesday, December 2, 2009

Saturday, November 28, 2009

Friday, November 27, 2009

Rate Hikes and Falling 3 Month Yields

After a sharp rate hike, yields fall as the economy goes into a recession.

Sunday, November 22, 2009

Thursday, November 19, 2009

More on the dangers of demand maintenance

The class struggle is who gets how much of output, or how much of per-capita output the median wage can buy.

If the ratio of per-capita output/median wage increases, then you have benefitted high earners and rentiers. If the ratio decreases, you have benefited "the average" worker. Just as employers cut labor hours to protect their financial holdings, so workers do not spend to increase their financial holdings. One wants to push the price of labor down, and the other wants to push the price of output down.

If the government steps in and purchases unwanted labor at a low support price, but purchases unwanted output at the market price, then it is systematically benefiting one side over the other. And it does not matter whether government is purchasing the output directly or via a benefit payment to labor. Unless 100% of government funded purchases result in wage boosts, you are still allowing capital to sell inventory to workers at prices higher than their wages allow, and end up anchoring median wages at a lower level in relation to output. As you continue this policy, the result is that the average wage can purchase less and less output, and the cost of living for the average worker increases, even though the price level need not. A slave society can have full employment and output.

If the ratio of per-capita output/median wage increases, then you have benefitted high earners and rentiers. If the ratio decreases, you have benefited "the average" worker. Just as employers cut labor hours to protect their financial holdings, so workers do not spend to increase their financial holdings. One wants to push the price of labor down, and the other wants to push the price of output down.

If the government steps in and purchases unwanted labor at a low support price, but purchases unwanted output at the market price, then it is systematically benefiting one side over the other. And it does not matter whether government is purchasing the output directly or via a benefit payment to labor. Unless 100% of government funded purchases result in wage boosts, you are still allowing capital to sell inventory to workers at prices higher than their wages allow, and end up anchoring median wages at a lower level in relation to output. As you continue this policy, the result is that the average wage can purchase less and less output, and the cost of living for the average worker increases, even though the price level need not. A slave society can have full employment and output.

Monday, November 16, 2009

Dangers of Demand Management Policies

To the degree that recessions are attempts by the public to save, then this is done for a reason. Typically that they are not being paid enough in wages to purchase output. If the government steps in and buys output on their behalf, or boosts wages via tax-breaks for workers, then this allows demand to become disconnected from wages.

So if there is going to be a demand-maintenance policy, then government needs at the same time to have wage maintenance policies, in the form of highly progressive tax-rates, excess profit rates, etc.

Recessions are natures way of setting fire to profits and asset prices because they are not supported by the wages of employees. If we are to prevent these fires, then we need to also institute controlled burns via tax policies.

So if there is going to be a demand-maintenance policy, then government needs at the same time to have wage maintenance policies, in the form of highly progressive tax-rates, excess profit rates, etc.

Recessions are natures way of setting fire to profits and asset prices because they are not supported by the wages of employees. If we are to prevent these fires, then we need to also institute controlled burns via tax policies.

Wednesday, October 28, 2009

Should the "natural rate" of interest be zero?

The argument for a zero risk-free rate goes as follows:

- It is immoral to allow a rentier to earn a risk free return. A nonzero Fed Funds rate allows this.

- The Loanable Funds model is incorrect: the interest rate does not balance savings and investment

- Existing Taylor rule type techniques are not very good.

- The government needs to be in a net deficit position in order to meet the savings needs of the private sector. If this is the case, then the call money rate will fall to zero unless the government "supports it" by draining cash.

- Therefore we should not drain cash and let the interest rate fall to zero.

My initial take on this is #5 does not follow from 1-4. The rate should be zero only if it overall welfare maximizing, and the rate should not be zero if it is not overall welfare maximizing.

In this post, I'll look at assertion #1.

I think this is basically a confusion about how the financial markets work. It's helpful here to disaggregate between the domestic private non-financial and domestic private financial sectors (e.g. "banks" and "investors").

The following charts the real MZM Own Rate and the real FedFunds rate:

The MZM Own Rate is the asset-weighted return earned by deposits immediately available for withdrawal. These are primarily (but not always) government insured, and so this rate is a good proxy for gauging the return available to investors in exchange for not parting with liquidity and not incurring risk. That return has averaged -1.89% since the start of the time series. There is some evidence that when the FedFunds was too high and when the FedFunds was too low, that the real return was positive. As MZM will be required to pay something to depositors, as the deposits do have a nonzero value to banks, a zero FedFunds rate would guarantee a positive risk-free return, whereas a non-zero FedFunds rate is generally associated with a negative risk-free return.

Perhaps the FedFunds rate is somehow causing returns to be higher than they otherwise "should" be, if it were zero. I think this is a confusion about what drives returns.

The long term return on equity (dividends + capital gain) is the GDP growth rate. However, there is a lot of volatility and a long term capital commitment is required to be able to reliably obtain this return. In exchange for a reduced level of capital commitment and less volatility, investors relinquish some yield and purchase bonds or other instruments. The reduction in yield is a function of changing investor preferences. Investors do not have the option of accessing money at the FedFunds rate. As the level of capital commitment decreases, the rate of return declines to the level of MZM, not to the FedFunds rate. The latter is an overnight rate reserved for banks.

Banks, on the other hand, do have the option of earning (on their excess reserves) the overnight rate, and of course they must also pay that rate. Here, there are no "moral" issues, since we are not talking about rentiers extracting money from productive society, but of bankers extracting money from each other. The purpose of the rate is to put a floor under the banks' cost of capital.

But still, aren't those costs passed onto the borrowers, who are forced to pay higher interest rates? Isn't this a moral issue?

That depends on whether you believe that there is a moral imperative for borrowers to have cheap access to loans. I will get back to that. In any event, banks will always charge a premium to borrowers as some loans will not perform, and the reality is that neither banks nor regulators can predict the tail end of distributions. Therefore the FedFunds rate serves as an additional safety valve, forcing the banks to be somewhat more conservative in their loan loss estimates than would be the case if their cost of capital were lower. But the difference is slight. If the banks cost of capital is 5%, and the bank has a capital requirement of 12:1, then $1 of capital can still fund $12 of loans, and this means that the bank must charge a premium of at least .05/12 or 0.4% more than it otherwise would if the FedFunds rate was zero. But if only $2 were borrowed, then the bank would need to charge a premium of 2.5%.

But herein lies the rub. Bank lending is driven by the consumers demand to borrow, not the bank's desire to lend. So the number of loans per dollar of capital changes, and if the cost of capital were to remain constant, then this premium would shift, and this would be disruptive to consumers. So this rate should fall when the demand for loans falls, and it should increase when the demand for loans increases, in order to keep the premium per loan constant.

At the same time, the safety valve itself may need to change due to changing collateral values and charge off rates.

The FedFunds rate is a floor on the banks' cost of capital, which can be thought of as a function of the FedFunds rate + various risk premia. If those risk premia increase, then in order to keep the loan cost to customers constant, the FedFunds rate would need to fall. If those premia decrease, the rate would need to rise.

All of the above are arguments that the FedFunds should be variable if lending rates are to be managed. But should they be managed? Perhaps we should let lending rates rise and fall based on the market's willingness to fund bank capital and willingness of borrowers to borrow. Here there are two key insights

- changes or shocks to the interest rate can be much more harmful than the rates themselves, primarily the risk is in upward spikes of borrowing rates, meaning that the government needs a tool to quickly lower the rates paid by customers much more than a tool to keep the rate low.

- The Level of interest rate plays a key role in determining the relative prices of a narrow set of assets within the economy, particularly houses. When it comes to the bulk of assets for which loans are made, there is no economic benefit to having the interest rate be high or low, other than the rate should be held constant or adjusted to "smooth" demand for the item.

Bank lending is primarily a real estate phenomena -- the Schumpeterian hero that borrows in order to expand capacity and innovate does appear in history, but is a statistical discrepancy in the flow of funds. The majority of productive investment is funded by retained earnings. Almost all loans are issued for: residential real estate, condos, apartment complexes, shopping centers, etc.. To a lesser degree there are loans for the purchase of consumer durables and college tuition.

The key thing to notice here is that the vast majority of loans are made on assets that do not produce a stream of cash-flows at all, and there is deep ambiguity about how to "value" a house, car, or a college education. Therefore the credit available to fund these expenditures, given a level of demand, will determine their price. So if you believe that there is value in smoothing demand for these assets, and that there is a social cost to be born by these assets being expensive relative to other assets in the economy, then you should believe in a non-zero bank cost of capital that adjusts in opposition to borrowing demand.

Sunday, October 25, 2009

The Fundamental Asymmetry

At the micro-level, there are incentives to increase productivity and decrease unit labor costs, paying workers less for each unit of output. But the costs of this -- decreased incomes to purchase inventory, are spread around. The only "incentive" that the market has to offer is an overall decline in sales in the form of a demand-led recession. There is no individual incentive to raise unit labor costs.

With the introduction of debt-financing, if accompanied by falling interest rates, even that asymmetrical incentive can be delayed, ushering in long booms of high profits, low inflation (since unit labor costs are low), and a significant deterioration in wages and an explosion in household borrowing. The main mechanism of household borrowing is for housing, and to a lesser degree, education -- both things that seem like assets but do not have a directly observable return. Once borrowing for these ends, the economy finds itself in a free-fall as businesses can no longer clear inventory.

If government stimulus spending is oriented towards purchasing inventory -- being in effect the consumer of last resort, then the key issue -- low wages -- will not be addressed and the result can be increasing unemployment even as total sales increase. If government spending is oriented towards boosting wages, either with a payroll tax holiday or directly employing the unemployed at high wages, then unit labor costs can be raised and workers can get back into a situation in which inventory clears without the need for households to take on more debt.

Saturday, October 24, 2009

Lincoln Senate Address on Monetary Policy

From Kansas City

Money is the creature of law, and the creation of the original issue of money should be maintained as the exclusive monopoly of national government. Money possesses no value to the state other than that given to it by circulation.

Capital has its proper place and is entitled to every protection. The wages of men should be recognized in the structure of and in the social order as more important than the wages of money.

No duty is more imperative for the government than the duty it owes the people to furnish them with a sound and uniform currency, and of regulating the circulation of the medium of exchange so that labour will be protected from a vicious currency, and commerce will be facilitated by cheap and safe exchanges.

The available supply of gold and silver being wholly inadequate to permit the issuance of coins of intrinsic value or paper currency convertible into coin in the volume required to serve the needs of the People, some other basis for the issue of currency must be developed, and some means other than that of convertibility into coin must be developed to prevent undue fluctuation in the value of paper currency or any other substitute for money of intrinsic value that may come into use.

The monetary needs of increasing numbers of people advancing towards higher standards of living can and should be met by the government. Such needs can be met by the issue of national currency and credit through the operation of a national banking system. The circulation of a medium of exchange issued and backed by the government can be properly regulated and redundancy of issue avoided by withdrawing from circulation such amounts as may be necessary by taxation, re-deposit and otherwise. Government has the power to regulate the currency and credit of the nation.

Government should stand behind its currency and credit and the bank deposits of the nation. No individual should suffer a loss of money through depreciation or inflated currency or Bank bankruptcy.

Government, possessing the power to create and issue currency and credit as money and enjoying the right to withdraw both currency and credit from circulation by taxation and otherwise, need not and should not borrow capital at interest as a means of financing government work and public enterprise. The government should create, issue and circulate all the currency and credit needed to satisfy the spending power of the government and the buying power of consumers. The privilege of creating and issuing money is not only the supreme prerogative of government, but it is the government's greatest creative opportunity.

By the adoption of these principles, the long-felt want for a uniform medium will be satisfied. The taxpayers will be saved immense sums of interest, discounts, and exchanges. The financing of all public enterprises, the maintenance of stable government and ordered progress, and the conduct of the Treasury will become matters of practical administration. The people can and will be furnished with a currency as safe as their own government. Money will cease to be the master and become the servant of humanity. Democracy will rise superior to the money power.

Abraham Lincoln, Senate document 23, Page 91. 1865.

Good Trade and Bad Trade

If we are off-shoring low-value add activities, and the freed up labor is used for higher value-add activities, then compensation would rise. Conversely if we are off-shoring high-value add activities, and the labor is freed up to work as Walmart greeters, then compensation would fall.

More at The Other Cannon.

Unit Labor Costs and Inflation

For those worried about hyperinflation, it's good to keep in mind that inflation is not caused by "printing money" in and of itself, or by an increase in wages. You need high wages per output, or high unit labor costs (ULC):

Sunday, September 20, 2009

Why borrow? Rational Expectations Redux and why nominal prices matter

Unrealized capital gains were a particularly important factor in the increase in net worth over the 2004–07 period. The share of total assets attributable to unrealized capital gains from real estate, businesses, stocks, or mutual funds rose 5.1 percentage points, to 35.8 percent in 2007. Although the level of debt owed by families rose noticeably, debt as a percentage of assets was little changed. The largest percentage change in debt was in borrowing for residential real estate other than a primary residence.From the 2007 Survey of Consumer Finances. Emphasis added.

With median and mean debt advancing faster than income, payments relative to income might be expected to increase substantially. In fact, total payments relative to total income barely increased, and the median of payments relative to income rose at a slower pace than it did between 2001 and 2004. Nonetheless, the share of families with high payments relative to their incomes increased notably.

Yet more evidence, together with the Permanent Income Hypothesis, that people look at their earnings power over time as an asset, just as any other asset, and their willingness to incur debt is due to how they price that earning-asset (together with their financial assets). A house is a 30 year commitment -- so you need to estimate 30 years of wages, discounted by both inflation and the risk of volatility in those wages. Same thing for other durables, and this percolates into day-to-day spending as well. "Flexible wages" are deeply destabilizing, as assets with volatile earnings are priced lower than assets with reliable earnings. Flexible wages would cause a further decrease in demand in excess of the actual change in wages.

Wednesday, September 16, 2009

Inequality and Debt growth

The following chart, taken from census data, shows the growth of income inequality since 1967:

The chart shows the share of national income for each cohort: bottom fifth, second fifth, third fifth, fourth fifth, top fifth and top 5%. You would expect the bottom fifth to collect a smaller share of income than the top fifth -- these ratios have been normalized so that 1967 =1. I.e. We assume 1967 is a "sustainable" level of inequality and track the increase that occurred since then.

Focusing on the third fifth, or "middle America", we can see the income gap from the decline in it's share of income from 1967 to 2008:

The next chart shows the growth of household debt/GDP since 1967 (i.e. we set the 1967 level to zero, and look at the increase that has occurred since then.) At the same time, we plot the running total of the income gap for the third fifth:

The growth in debt was a re-cycling mechanism, allowing the middle class to continue consuming (and hence maintain GDP growth) all while incomes fell. In other words, wages shifted from the middle incomes to top management/asset holders, while at the same time the purchasing power of the middle incomes was maintained by debt-financing. The increase in household debt funded the increased gains for the top incomes.

The total amount spent on wages did not change very much, but the distribution changed, effectively the top 1% earned much more, the top decile net of the top 1% stayed the same, and everyone else's wages collapsed.

In such an environment, if workers are paid less, they wont be able to purchase goods, demand will decrease, and therefore prices will fall to adjust, meaning lower profits for the owners of capital, and the income balance will be restored in real terms.

Debt-financing can be used as a mechanism to prevent this adjustment. As long as the debt is rolled over -- as long as consumers are willing to take on more debt -- inequality can grow and prices/profits will not adjust to reflect the lowered wages of average employees.

In this case, the asset base will swell, interest rates will fall, the debt stock will swell, and consumption will remain constant even as wages fall. That is, until a debt crisis occurs.

A similar dynamic can be seen with the current account. The Chinese government confiscates dollars from exporters, prints up RMB and "buys" those dollars at prescribed rates. The end result is that the people who produce goods suffer inflation as the goods are loaded on ships to disappear. As a result, the real purchasing power and consumption of the Chinese workers is suppresed, while U.S. workers are put under wage discipline. There is transfer of technology which helps China, but you can have technology transfer without suppressing wages. Again, debt-financing is used to bypass the market adjustment, this time of currencies as well as real wage rates in China.

This is the key macro-economic and political problem of our era -- debt-financing is being used to suppress wages, preventing necessary price adjustments from bursting the income concentrations, and this dynamic is fundamentally de-stabilizing.

But until we understand the root of the problem, we wont be able to address it. The problem isn't "Debt" in some abstract sense, and it certainly isn't "too much borrowing" in and of itself, since the borrowing was only an attempt to keep wages at their 1967 share of GDP. In other words, that middle quintile only borrowed enough to try buy their own domestic output. The problem is not paying workers enough money to maintain demand for the goods they produce. This is why we are suffering from chronic demand shortages, asset bubbles, abnormally low interest rates, record inequality, and crushing private debt.

Tuesday, September 15, 2009

For every invested dollar...

... almost 80 cents goes to pay the salaries, bonuses, and other benefits of employees in the Financial Services and Insurance Industries.

... almost 80 cents goes to pay the salaries, bonuses, and other benefits of employees in the Financial Services and Insurance Industries. "Domestic Investment" is defined as gross investment exenditures by both the government and private sectors net of depreciation. "Finance and Insurance" compensation consists of BEA FIRE compensation data net of real estate sector compensation.

Monday, September 14, 2009

Whose government is it?

You can tell the priorities of government by looking at what it is trying to optimize.

China is printing RMB like no tomorrow, so that they can sterilize dollar inflows and keep exporting. They are interested in developing domestic capital: skills, a trained workforce, technology transfers, research and development, viability of the business sphere and full employment.

Reading Keynes, the emphasis was always on maintaining full employment. Then the emphasis shifted to total output growth. And since then the emphasis has shifted to protecting bondholders and keeping inflation and interest rates low.

We are protecting and bailing out bondholders, not investing in our capital base or fighting to build the tangible things that create wealth for the future: better infrastructure, education, research, stable business profits and high wages.

Any government that is more concerned with inflation and interest rates than with employment and business development has been taken over by the illusion that financial wealth is equivalent to real wealth.

Sunday, September 13, 2009

The Price/Earnings Ceiling

From the valuation approach described previously, we can look at the earnings yield of a broad index such as the SP 500 and invert the growth formula:

earnings yield = dividend yield + growth rateto obtain:

P/E = 1/(dividend yield + growth rate)To put an upper bound on the P/E ratio, we want a lower bound on the yield + growth rate. Generally speaking, the total returns on capital (for equities, that would be growth rate and dividends) have been the GDP growth rate over the period. That is one of Kaldor's "stylized facts", which actually says that returns to capital as a fraction of GDP are the same over time, and that therefore the growth rate will be the same. Now, that doesn't need to be in equity, it could be in other forms of capital, but over time, it's hard for the equity returns to outgrow the total returns.

If you don't like the Kaldor argument, then notice that GDP = GNI, so that if national incomes are growing at g, people will be willing to accept effective bond rates of a little below g, so that the premium for equity should be a little higher than that. So that gives g as the expected returns from capital.

So that gives a long run upper bound (actually approximate equality) for the P/E multiple for the equity market as a whole. Obviously the variance is large :) Going forward, output growth may continue to slow.

Suppose you think a GDP growth rate of only 4% (nominal) is warranted over the next 20 years. In that case, the average P/E multiple would be at most 25, but there is a good chance that the equity markets wont like such a low yield, and money will shift to other forms of capital.

This surprises people who associate "high multiples" with growth stocks, but that is only to the degree that their multiple is higher than that of the index. The economy as a whole grows with GDP, as does the return to equity capital as a whole. Some specific returns may be more highly valued, but if the entire index is more highly or lowly valued than the yield available for the economy, then you are looking at a bubble or arbitrage opportunity. Historically 10 years has been long enough for this to unwind, and 20 years certainly has.

The larger the deviation, the more difficult it is to maintain earning growth as the company grows. For the SP 500 as a whole, if it is a constant share of capital, then the multiple will increase in absolute terms as yields fall.

It is usually better to buy when earnings are collapsing, but in this case you look at "smoothed" 10 year earning multiples (i.e. the current price divided by the average real earnings over the last 10 years). This would allow you to not be fooled into thinking that a high multiple is expensive, when in reality the denominator is abnormally low. Alternately, smoothing will not let you think that anything goes -- for example the July 2009 multiple was 117 -- and the market kept climbing.

FYI, in July '09, the smoothed P/E multiple was about 18. Not cheap by any means, and certainly not sustainable, unless you are assuming something along the lines of a dividend yield of 2% and nominal earning growth rates of 3.5% going forward. In that case, it might not have been a bad idea to buy. Just be aware that a high multiple is only justified on a long term basis only if we experience a secular growth collapse that also would also result in long term bond yields falling to well below 3.5% as well. Such an environment might not fare well for equities.

Saturday, September 12, 2009

Negative Re-Investment Rates

When the cost of equity capital is low, then the re-investment rate is high. This is dangerous for firms because the market is fickle, and periods of complacency quickly turn into panics, at which point the capital is re-priced, and now higher returns are demanded. Companies respond to this by trying to defend their dividends and thus end up liquidating a portion of their capital stock in the form of layoffs, shutdowns, and other asset sales.

You can see a historic negative re-investment rate in this graph, corresponding to capital liquidation for the market as a whole.

Note that this is different from lowering the re-investment rate as you would expect in a regular recession. As long as the re-investment rate is positive, then productive capacity is still being increased, but at a lower rate. I.e., the growth of productive capacity is "slowing down" as opposed to shrinking.

Layoffs are always occuring as is hiring, but when the market as a whole has a negative re-investment rate, then productive capacity as a whole is decreasing. You can think of the difference as that between laying off a few workers versus closing a factory. It is harder for employment in the latter case to recover because it requires a greater investment commitment on the part of management as they emerge from the recession. But this is exactly when management is still skittish. This is not to say that employment can't or wont recover -- but the hurdle will be higher.

Moreover, the graph suggests that the current market downturn is fundamentally different from the crashes and recessions in earlier periods. You have to go back to Great Depression, the 1921 recession, or the Long Depression (1893-1898) to find such periods of negative re-investment, and all of those periods were dwarfed by the negative re-investment that we see today. Note that all three of the historical precedents were deflationary recessions.

Valuing Equities without Discounting

In the diagram above, each time a firm generates profits (earnings), a portion are paid out as a dividend, and the remainder are re-invested, adding to the firm's capital stock. Assuming that the firm is on a stable growth trajectory, then the various multiples (price to earnings or price to dividend) should be constant over time, while the earnings, dividend, and market cap should grow with some real growth rate, g. If this were not the case, these multiples would go to zero or to infinity over time.

By "real growth rate", I mean the logarithmic derivative (i.e. (1/x)dx/dt = g). Now let r be the re-investment ratio:

r*earnings = retained earings = earnings - dividend

In particular, if r = 1, then all earnings are re-invested, and if r is negative, then the firm is selling off capital, since it cannot meet the owners' required rate of return.

Then the growth rate of capital (dC/dt) is just rE -- the amount re-invested. Therefore the "real growth rate" is rE/C, so that we have

g = rE/C = r*(E/C) = r*(earnings yield)

Which we can re-arrange to read:

dividend yield = ((1-r)/r)*g= (1/r-1)*g

earnings yield = g/r

earnings yield – dividend_yield = g

earnings yield = dividend yield + g ("dividend capitalization model")

- g = growth rate of earnings, dividends, market-cap

- r = re-investment ratio

This allows us to value equities without discounting infinite sums -- by defining steady-state ratios. The assumption is only one of stability (which the discounted sums approach also requires). In order to value a company, you need to estimate the earnings growth rate as well as the dividend yield (or the re-investment ratio). This gives the standard "dividend discount" valuation approach, although the method here is a bit more general, in that no dividends need to be paid -- full re-investment is also allowed.

Now, in the real world, the market doesn't know how much to value capital -- that is a difficult problem and so the market value oscillates around the "true" value, as investors constantly adjust their expectations based on optimism and pessimism, excessively marking down the value of capital during busts, and over-valuing capital during booms. To see these mood swings, consider the following:

This chart graphs the stable growth path, g, obtained by taking the 10 year average earnings-yield and the present dividend yield. It then graphs the 10-year trailing average of the observed earnings growth.

You can see that there are turning points, in which the actual earnings growth (blue) wildly overshoot and undershoot. These are equivalent to "earnings booms" and "earnings busts", in which the earnings grow much faster or slower than the required growth rate as determined from a 10 year backwards-looking window. These correspond to secular booms and busts in corporate profits, and are influenced not just by changes in output, but by debt-fueled demand, tax law changes, access to new markets, etc.

In general, expectations formation is backwards looking but there are real turning points -- changes in mood about the future (such as the Great Depression or the post-war boom) that a purely backward looking metric will not detect. Also note that the booms and busts are secular -- they last much longer than simple recessions, so that large multiples seem normal, until the next collapse and re-pricing, or until the next boom occurs.

Wednesday, September 9, 2009

Chart of the Day: Earnings Arbitrage in Financial Yields/Private Sector Yields

When financial yields are low, price to book ratios are high, so the businesses represented in the financial markets are expensive. This should encourage investment in things like proprietorships and non-corporate business. When yields are high, then price-to-book ratios are low, and the reverse is true -- why futz around with Sally's Shoe Store when Johnson and Johnson is yielding 6%?

The following chart from the NIPA table 2.1 plots personal income received from financial assets (dividend and interest payments) against personal income received from proprietorships, both farm and non-farm. The latter attempts to exclude wages and operating income and tries to account for depreciation and inventory changes -- this is "return on capital" for proprietorships, which are classified and non-corporate farm and non-farm non-corporate businesses that must file certain tax forms that I don't care about. Note that rental income received is a separate type of income and is not shown (it moves uniformly up, from left to right, but there are owner-equivalent rent issues there). Both time series are presented as ratios of GNI.

The sum of both time series is shown below:

See how these returns began to decline during the debt-deflation and climbed during the debt-inflation starting in the 1980s, but there is at least evidence for not a lot of variation for the sum of earnings for both corporate and non-corporate businesses.

Monday, September 7, 2009

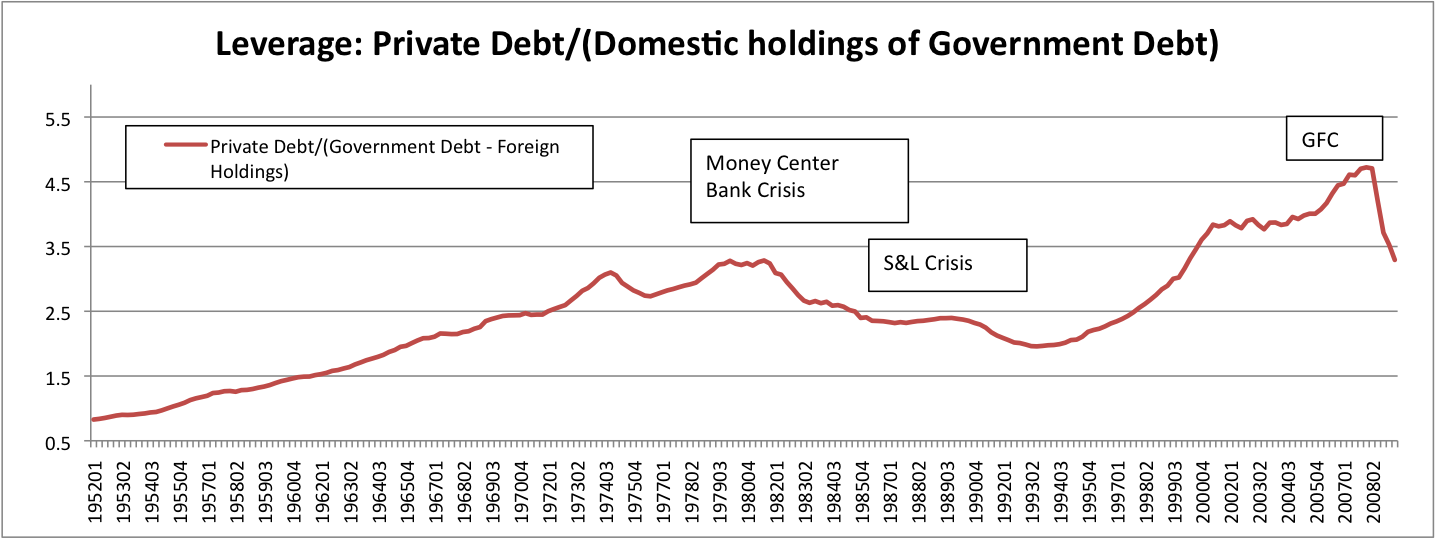

Gloomy Chart of the Day

It seems that you can only pay down one sector's debt to GDP at the expense of increasing another's -- that is, except for mass defaults. This chart omits a few sectors, such as farm debt, and nonfarm non-corporate business debt, but the sum of non-financial private sector debt/GDP + the sum of government debt/GDP has always been growing, too -- ever since "Fed Independence Day", when the U.S. stopped forcing the Fed to monetize whenever treasury yields rose above a certain level.

In particular, the chart suggests that the paydown of Federal debt that occurred in the post-war period came at the expense of an increase in household debt, and to a lesser degree business debt. The current miniscule drop in household debt is coming at the expense of a significant increase in Federal debt, and to a lesser extent, (corporate) business debt. The source is The Federal Reserve's Flow of Funds, and the time period is from Q1 1952 to Q1 2009.

Sunday, September 6, 2009

A Tale of Nine Cities: Rents 1930-2007

The following continues the historical exploration of relative house prices by looking at the ratio of median rents paid in nine selected California cities to the ratio of median rents throughout the state. The state ratio takes into account urban areas only (rural median rents are lower). All data comes from the census.

Saturday, September 5, 2009

Rare voice of reason

Simple, honest, well-reasoned and bound-to-be-ignored post:

I will paraphrase from an influential article by Clay Shirky, with my changes in italics :)

Revolutions create a curious inversion of perception. In ordinary times, people who do no more than describe the world around them are seen as pragmatists, while those who imagine fabulous alternative futures are viewed as radicals. The last couple of decades haven’t been ordinary, however. Inside thepapersnation, the pragmatists were the ones simply looking out the window and noticing that the real world was increasingly resembling the unthinkable scenario. These people were treated as if they were barking mad. Meanwhile the people spinning visions ofpopular walled gardens and enthusiastic micropayment adoptionschemes to repackage bad assets into good assets, visions unsupported by reality, were regarded not as charlatans but saviors.

Friday, September 4, 2009

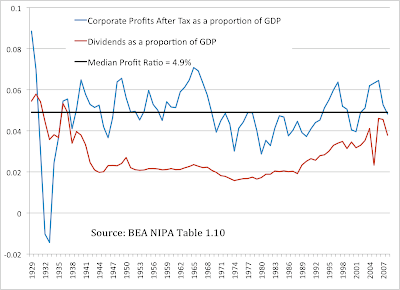

Another Look at Long Run Equity Returns

Earlier I mentioned how the market cap growth of companies cannot outpace GDP growth -- except for brief periods of multiple expansion. Here is a chart from 1929 to 2008 showing the total net operating profits after taxes together with dividend payouts of U.S. Corporations divided by Gross National Income (the data comes from the BEA):

Over this time period, the ratio of profits available to corporate business was around 5% of the economy. There is what seems to be obvious mean-reversion. More interesting is the stability of the dividend payouts except for the two credit bubble periods, one deflating since 1929, and one inflating from the 1980s until just recently. Companies are loathe to increase dividends without appropriate future coverage, and so the dividend payout/GNI contains meaningful information about the estimates of management for sustainable future returns, and is much less volatile than the equity multiple. A dividend payout of 2% of GNI was remarkably stable between the two credit bubbles.

Don't let anyone fool you into believing that the total equity value of U.S. corporations can consistently outpace the size of the economy. As can be seen from the historical record, periods of multiple expansion for both corporate profits/GNI as well as market-cap/GNI tend to mean-revert, even though they can last long enough to convince the public that "this time it's different". Those who cut their teeth in the period from 1980-2000 did not experience a representative time in the history of U.S. equity values.

Over this time period, the ratio of profits available to corporate business was around 5% of the economy. There is what seems to be obvious mean-reversion. More interesting is the stability of the dividend payouts except for the two credit bubble periods, one deflating since 1929, and one inflating from the 1980s until just recently. Companies are loathe to increase dividends without appropriate future coverage, and so the dividend payout/GNI contains meaningful information about the estimates of management for sustainable future returns, and is much less volatile than the equity multiple. A dividend payout of 2% of GNI was remarkably stable between the two credit bubbles.

Early data about market capitalization is hard to find, but we can look at total market capitalization in the second half of the 20th century. The following chart, from the Federal Reserve Flow of Funds, shows total market capitalization of U.S. corporations divided by the Gross National Income, reported on a quarterly basis. You can also see the total dividend payouts divided by the total market cap (i.e. the dividend yield of the entire market).

By this historical metric, the present market is not cheap. It would need to fall by 50% in order to reach the post-war lows from 1974-1984 -- and that is a decade long period! We can also see the same shape that is a common refrain in most of the graphs: the 20 year run-up culminating to the twin-peak blow off of 2000 and 2007 that at least seem to suggest the beginning of a downtrend. From this long-run perspective, the period from 2003-2007 seems like an enormous bear market rally.

Don't let anyone fool you into believing that the total equity value of U.S. corporations can consistently outpace the size of the economy. As can be seen from the historical record, periods of multiple expansion for both corporate profits/GNI as well as market-cap/GNI tend to mean-revert, even though they can last long enough to convince the public that "this time it's different". Those who cut their teeth in the period from 1980-2000 did not experience a representative time in the history of U.S. equity values.

Historically, the Market Cap of U.S. Corporations averaged approximately the size of GNI (actually 0.94xGNI), although it did swing around this value. The following chart shows the actual 10 year returns of purchasing a slice of equity, together with the predictions of 2 estimates.

The 10-year forward equity returns have been the worst on record in the postwar period.

The first estimate assumes 100% reversion in a 10 year time period, with the assumption that GDP growth will be the value of the current 10 year treasury. The second line assumes 50% reversion to the 0.94xGDP value, also assuming that 10 year forward GDP growth will be equal to the 10 year treasury rate. Of course, no one can tell when or to what extent mean-reversion will occur. This type of analysis is a crude version of John Hussman's analysis, with the notable exception that I am using the 10 year treasury estimate of GDP as opposed to a constant 6% GDP growth trend, I'm excluding dividends in the total return calculation, and am selecting the parameters not by fixed P/E terminal multiples, but by proportion of trend reversion. The interested reader can make each of these adjustments themselves -- the purpose here is not to predict market values, as it is hard to out-guess the crowd, but to provide a sense of valuation for the market as a whole -- what does a dollar of equity buy today in comparison to what it bought yesterday? Moreover, if the present multiples were to mean-revert, then what would the market cap be? These types of considerations should inform those who don't always believe that we are in a new era.

Both estimates currently predict annualized returns of approximately 3% (excluding dividends), over a 10 year period. These are all nominal returns, but the Old Barkeep is not too worried about inflation over the next decade. I hope to return to this theme with some more sophisticated models.

Thursday, September 3, 2009

In Search Of The California "Desirability Premium"

Housing is more expensive in more "desirable" areas -- that's a bit of a tautology, of course, since we don't have a way of measuring how desirable an area is, and having high paying jobs will certainly attract more people, in which case they will be willing to bid up the cost of housing in order to access that labor market.

But in more desirable areas, are owners willing to pay a greater proportion of their income on housing? Let's take a look:

FYI, owners are willing to devote a median value of 31% of their household income for mortgage costs in San Francisco, 35% in Oakland, 34% in Los Angeles, 29% in Vacaville, 44% in Beverly Hills, and 40% in Lennox. In general, the graph suggests a slight downtrend, in that owners in wealthier areas are willing to devote a slightly smaller share of their income for mortgage costs, however the R^2 value does not give a lot of confidence.

In this case, there is an extremely weak correlation that suggests that the greater the inequality, the less owners are willing to pay, proportionately -- but the relationship is weak.

So it turns out that the "desirability premium" is very hard to find when looking at data. Generally speaking, areas with higher household incomes command higher house prices, but not as a percentage of income. There is evidence that as incomes increase, people are willing to spend less, proportionate to their income, on monthly mortgage costs.

But in more desirable areas, are owners willing to pay a greater proportion of their income on housing? Let's take a look:

Source: American Community Survey 2005-2007 3-Year Estimate

Our universe consists of all census "places" -- cities or townships -- in California. The x-axis shows the per-capita income for each place, while the Y-axis measures the median percentage of income that mortgage holders are willing to pay. "Mortgage costs" here also include other ownership costs such as property taxes and utilities.

FYI, owners are willing to devote a median value of 31% of their household income for mortgage costs in San Francisco, 35% in Oakland, 34% in Los Angeles, 29% in Vacaville, 44% in Beverly Hills, and 40% in Lennox. In general, the graph suggests a slight downtrend, in that owners in wealthier areas are willing to devote a slightly smaller share of their income for mortgage costs, however the R^2 value does not give a lot of confidence.

But ownership rates vary -- in San Francisco, only about 1/3 of the housing stock is owner occupied, whereas the state average is much higher. Let's look at the relationship between ownership rates and mortgage burdens:

Source: American Community Survey 2005-2007 3 Year Estimate

Here there is some evidence that ownership burdens increase somewhat as ownership rates fall -- by 0.65% for every 10% decline in ownership rate -- but again the R^2 doesn't give confidence and the drop is slight.

Perhaps it's more a question of inequality -- in areas with high income inequality, owners might be willing to pay a premium to showcase their status:

Source: American Community Survey 2005-2007 3 Year Estimate

In this case, there is an extremely weak correlation that suggests that the greater the inequality, the less owners are willing to pay, proportionately -- but the relationship is weak.

So it turns out that the "desirability premium" is very hard to find when looking at data. Generally speaking, areas with higher household incomes command higher house prices, but not as a percentage of income. There is evidence that as incomes increase, people are willing to spend less, proportionate to their income, on monthly mortgage costs.

Wednesday, September 2, 2009

A Tale of Six Cities: 1930-2007

Source: Census

The chart shows the ratio of the median house price to the median annual rent paid for six california cities form 1930-2007, using census data together with the American Community Survey. Rents are calculated as median monthly contract rent x12.

You can see both the wage compression period, together with a secular period of expanding multiples (and declining yields). This is due to effects such as Proposition 13, the mortgage interest deduction, longer repayment periods and the introduction of additional subsidies. Don't forget the boom/bust pattern common to California, particularly coastal California, as well as the parabolic multiple increase starting with the 2000 census. The time series ends in 2007, but we can watch it collapse as subsequent surveys are released.

A Tale of Seven Cities: 1930-2007

The following tracks the ratio of city median rents to state median rents for seven California cities. Note that "median rent" means median contract rent paid -- not asking rent. The data is from the decadal census, together with the American Community Survey.

Source: Census

Note the rent uptick during the dot-com period followed by collapse for San Francisco and San Jose, although Oakland had a very brief mini-spike as well. Also note the effects of wage compression during the post war period, as rents crowded around 1 and then diverged. Also note the increasing volatility of these ratios, as the higher income cities tend to be more volatile after the period of wage compression.

Can you guess when rent control was instituted in some of these cities?

Long Run San Francisco House Prices: 1930-2007

This chart shows the ratio of the median price of a San Francisco owner occupied house to the median price of a California owner occupied house. Census data for selected years 1930-2007.

Source: Census

The spike peaking in 2001 represents the dot-com era -- the first hump of the income bubble. The fall from the spike is not due to San Francisco prices adjusting downward, but to California prices shooting upward. By 2006, prices in California caught up with San Francisco, but by 2007, prices in California began to fall again as the housing bubble deflated in the suburban areas of the state. Unfortunately there is a 2 year lag for releasing the American Community Survey, so we will see what happens to that spike going forward. I predict another spike, followed by a reversion to the long run trend.

The San Francisco Income Bubble

The Old Barkeep is fascinated by the insanity of San Francisco's housing market, and demographic shifts generally. Always a rich town, the city has recently experienced a big income boost -- can you recognize the pattern from 1997-2007?

Source: BEA Regional Accounts

There is a 2 year lag for the local data, but I don't think this bump is durable. Let's see what that graph looks like once the 2009 numbers come out.

Tuesday, September 1, 2009

Goosing Equity Returns via Dividend Re-investment?

The Old Barkeep is not impressed with various book peddlers and optimists advertising the possibility of high "total" returns in excess of GDP growth.

Here is the algorithm:

First, some background.

The market cap of a firm reflects investors' beliefs about the present value of all future earnings of that firm. Some of those earnings are retained -- re-invested by the management -- and the remainder are classified as "surplus profits" and are distributed as dividends.

The decision to make a distribution amounts to a belief by the firm that it cannot re-invest those profits while maintaining the expected growth rate -- so it distributes those dividends to investors.

On the ex-dividend date, the equity value falls by the distribution amount -- since the "value" of the company is now less (it has one less future earning!), and on the distribution date, the owners receive a cash payment.

The total value of the owners' stake has not changed, they just have some of that value in the form of cash that they control as opposed to having that cash locked up in their equity accounts. For this reason, you do need to include cash-holdings in any calculation of total return. A total return calculation should include all holdings.

In the real world, some of those dividends are re-invested in equities, and to the degree that they are, this drives up the equity value of target investments as investors compete to bid up the share price of the target firms. So the net effect is to lower the cost of capital for some firms while raising it for others as investors continually engage in a process of valuation.

This process supposedly results in no company being without sufficient capital to give investors the return they demand. So for the market as a whole, the dividends flowing out of the entire market are surplus profits for all the firms in the market. In other words, over time, investors believe that no company can increase its capital base while maintaining the expected yield; otherwise they would bid up the share price and drive down yield.

Therefore when looking at a historical time series of prices, whatever equity re-investments actually occurred, they are already recorded in the time series. It is double-counting to include the observed market cap increases of those firms that are the targets of investment, and to not count the market cap declines of firms that made distributions. Moreover, any dividends thrown out by the entire index should be assumed to be surplus capital for the index as a whole. This means, if those dividends were re-invested, they would come at the expense of a fall in yield.

Equity prices are everywhere and always subject to a process of valuation, and this means that you should not always re-invest. You cannot always throw surplus capital back into the hands of management and maintain the same rate of return. You cannot always bid the price of equity up and expect profits to rise. At some point, additional investment results in stock price bubbles followed by crashes, because the earnings growth rate is constrained by GDP growth rates, and you cannot goose GDP sustainably by bidding up the price of equity.

At some point, you are better off buying a bond or even holding the dividend in a cash-equivalent, rather than overpaying for low yield.

Now, the specific flaw in the algorithm: the mistake is in Step 3.

The book-peddler is inserting a fake transaction into the historical time series, by assuming that you will be able to increase your holdings of the company without bidding up the price. All these backwards looking "what-if" scenarios suffer from the same flaw, which is that they are minority strategies. If enough people followed these strategies, the price would shoot up, the dividend yield would collapse, and the strategy would underperform the historical time series. Any time you see someone peddling a "total return" strategy that is greater than long-run GDP growth (which was 6%, in nominal terms, over the last 100 years), then you are being sold snake oil.

How much does the fake transaction that allows for purchases of shares without bidding up the share price distort the historical time series? One way to measure this is that if the "average" investor's equity holding could grow, by any series of transactions at the rate of the dividend payout + the observed rate of equity growth, then the total equity value of the whole market would also grow faster than the observed rate (by the same amount). Moreover, the synthetic model assumes that the dividend yield on this larger equity value would be the historical yield. This means that there would be a divergence between the observed profits and the profits as predicted in the model:

Given that aggregate earnings grow at the rate of GDP growth, a strategy that claims to outperform GDP growth by 3%, will after 100 years predict

But, what about our investor, who suffered an equity loss of $1 and has $1 in his cash account? Can't we add $1 to his total returns? Absolutely! If by "total returns" you mean a real-time mark-to-market of all the holdings of a particular investor, then this is valid (and necessary) to gauge performance. And you should add total dividends paid to the cash account of any historical time-series. The only flaw is when you insert fake transactions into the historical time series, by assuming re-investment without assuming that this will change the historical prices -- i.e. assume it is possible to buy or sell shares without altering the historical prices. That is fundamentally a minority strategy, and will not succeed if engaged by the public at large, or even by a sizeable minority of the public. Certainly it will fail if large players such as pension funds use the strategy.

So, then, what are the expected "total returns" of the market?

Here is the algorithm:

- Start with a notional account. E.g. $1 in the DJIA index, invested in 1900

- Over each time period, if the index changes by X%, assume that your equity does, too.

- Over each time period, if a dividend payout of D% is given, add back that amount to the equity value, via a "dividend re-investment model".

- Watch your holdings increase at a compound annual growth rate in excess of the growth rate of the index.

- Peddle books, or drive a pension fund into the ground.

First, some background.

The market cap of a firm reflects investors' beliefs about the present value of all future earnings of that firm. Some of those earnings are retained -- re-invested by the management -- and the remainder are classified as "surplus profits" and are distributed as dividends.

The decision to make a distribution amounts to a belief by the firm that it cannot re-invest those profits while maintaining the expected growth rate -- so it distributes those dividends to investors.

On the ex-dividend date, the equity value falls by the distribution amount -- since the "value" of the company is now less (it has one less future earning!), and on the distribution date, the owners receive a cash payment.

The total value of the owners' stake has not changed, they just have some of that value in the form of cash that they control as opposed to having that cash locked up in their equity accounts. For this reason, you do need to include cash-holdings in any calculation of total return. A total return calculation should include all holdings.

In the real world, some of those dividends are re-invested in equities, and to the degree that they are, this drives up the equity value of target investments as investors compete to bid up the share price of the target firms. So the net effect is to lower the cost of capital for some firms while raising it for others as investors continually engage in a process of valuation.

This process supposedly results in no company being without sufficient capital to give investors the return they demand. So for the market as a whole, the dividends flowing out of the entire market are surplus profits for all the firms in the market. In other words, over time, investors believe that no company can increase its capital base while maintaining the expected yield; otherwise they would bid up the share price and drive down yield.

Therefore when looking at a historical time series of prices, whatever equity re-investments actually occurred, they are already recorded in the time series. It is double-counting to include the observed market cap increases of those firms that are the targets of investment, and to not count the market cap declines of firms that made distributions. Moreover, any dividends thrown out by the entire index should be assumed to be surplus capital for the index as a whole. This means, if those dividends were re-invested, they would come at the expense of a fall in yield.

Equity prices are everywhere and always subject to a process of valuation, and this means that you should not always re-invest. You cannot always throw surplus capital back into the hands of management and maintain the same rate of return. You cannot always bid the price of equity up and expect profits to rise. At some point, additional investment results in stock price bubbles followed by crashes, because the earnings growth rate is constrained by GDP growth rates, and you cannot goose GDP sustainably by bidding up the price of equity.

At some point, you are better off buying a bond or even holding the dividend in a cash-equivalent, rather than overpaying for low yield.

Now, the specific flaw in the algorithm: the mistake is in Step 3.

The book-peddler is inserting a fake transaction into the historical time series, by assuming that you will be able to increase your holdings of the company without bidding up the price. All these backwards looking "what-if" scenarios suffer from the same flaw, which is that they are minority strategies. If enough people followed these strategies, the price would shoot up, the dividend yield would collapse, and the strategy would underperform the historical time series. Any time you see someone peddling a "total return" strategy that is greater than long-run GDP growth (which was 6%, in nominal terms, over the last 100 years), then you are being sold snake oil.

How much does the fake transaction that allows for purchases of shares without bidding up the share price distort the historical time series? One way to measure this is that if the "average" investor's equity holding could grow, by any series of transactions at the rate of the dividend payout + the observed rate of equity growth, then the total equity value of the whole market would also grow faster than the observed rate (by the same amount). Moreover, the synthetic model assumes that the dividend yield on this larger equity value would be the historical yield. This means that there would be a divergence between the observed profits and the profits as predicted in the model:

Given that aggregate earnings grow at the rate of GDP growth, a strategy that claims to outperform GDP growth by 3%, will after 100 years predict

- dividend payments 19 times the observed payments

- market caps 19 times greater than the observed market caps

- "total returns" 19 times greater than the total returns of the average investor.

But, what about our investor, who suffered an equity loss of $1 and has $1 in his cash account? Can't we add $1 to his total returns? Absolutely! If by "total returns" you mean a real-time mark-to-market of all the holdings of a particular investor, then this is valid (and necessary) to gauge performance. And you should add total dividends paid to the cash account of any historical time-series. The only flaw is when you insert fake transactions into the historical time series, by assuming re-investment without assuming that this will change the historical prices -- i.e. assume it is possible to buy or sell shares without altering the historical prices. That is fundamentally a minority strategy, and will not succeed if engaged by the public at large, or even by a sizeable minority of the public. Certainly it will fail if large players such as pension funds use the strategy.

So, then, what are the expected "total returns" of the market?

- A first order long run estimate is the long run GDP growth estimate. This has been the observed returns over 50 year time periods, at least for equities.

- John Hussman authored an analysis that takes the "gap" between current stock values and the long run GDP growth rate, taken to be 6%, with the assumption that mean-reversion will occur in the longer run. There is evidence for this over 10 year time periods

Note that, in general, there is nothing wrong with specifying an asset allocation strategy in an attempt to outperform. Most try to outperform! Just be aware that any strategy promising returns in excess of GDP growth will be a minority strategy, that if followed by enough people, will fail to outperform.

Subscribe to:

Posts (Atom)