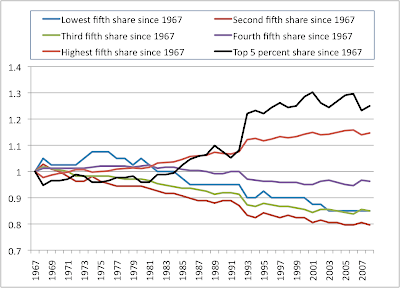

The following chart, taken from census data, shows the growth of income inequality since 1967:

The chart shows the share of national income for each cohort: bottom fifth, second fifth, third fifth, fourth fifth, top fifth and top 5%. You would expect the bottom fifth to collect a smaller share of income than the top fifth -- these ratios have been normalized so that 1967 =1. I.e. We assume 1967 is a "sustainable" level of inequality and track the increase that occurred since then.

Focusing on the third fifth, or "middle America", we can see the income gap from the decline in it's share of income from 1967 to 2008:

The next chart shows the growth of household debt/GDP since 1967 (i.e. we set the 1967 level to zero, and look at the increase that has occurred since then.) At the same time, we plot the running total of the income gap for the third fifth:

The growth in debt was a re-cycling mechanism, allowing the middle class to continue consuming (and hence maintain GDP growth) all while incomes fell. In other words, wages shifted from the middle incomes to top management/asset holders, while at the same time the purchasing power of the middle incomes was maintained by debt-financing. The increase in household debt funded the increased gains for the top incomes.

The total amount spent on wages did not change very much, but the distribution changed, effectively the top 1% earned much more, the top decile net of the top 1% stayed the same, and everyone else's wages collapsed.

In such an environment, if workers are paid less, they wont be able to purchase goods, demand will decrease, and therefore prices will fall to adjust, meaning lower profits for the owners of capital, and the income balance will be restored in real terms.

Debt-financing can be used as a mechanism to prevent this adjustment. As long as the debt is rolled over -- as long as consumers are willing to take on more debt -- inequality can grow and prices/profits will not adjust to reflect the lowered wages of average employees.

In this case, the asset base will swell, interest rates will fall, the debt stock will swell, and consumption will remain constant even as wages fall. That is, until a debt crisis occurs.

A similar dynamic can be seen with the current account. The Chinese government confiscates dollars from exporters, prints up RMB and "buys" those dollars at prescribed rates. The end result is that the people who produce goods suffer inflation as the goods are loaded on ships to disappear. As a result, the real purchasing power and consumption of the Chinese workers is suppresed, while U.S. workers are put under wage discipline. There is transfer of technology which helps China, but you can have technology transfer without suppressing wages. Again, debt-financing is used to bypass the market adjustment, this time of currencies as well as real wage rates in China.

This is the key macro-economic and political problem of our era -- debt-financing is being used to suppress wages, preventing necessary price adjustments from bursting the income concentrations, and this dynamic is fundamentally de-stabilizing.

But until we understand the root of the problem, we wont be able to address it. The problem isn't "Debt" in some abstract sense, and it certainly isn't "too much borrowing" in and of itself, since the borrowing was only an attempt to keep wages at their 1967 share of GDP. In other words, that middle quintile only borrowed enough to try buy their own domestic output. The problem is not paying workers enough money to maintain demand for the goods they produce. This is why we are suffering from chronic demand shortages, asset bubbles, abnormally low interest rates, record inequality, and crushing private debt.